UAE MOHRE Salary Payment Rule 2026: What Businesses Must Know About the New Payroll Compliance Requirements

EmaraTax Access Update: How to Access the UAE FTA EmaraTax Platform Through the Services Menu Important Update for UAE Businesses The Federal Tax Authority (FTA) has announced a navigation update to its official website, changing the way users access the EmaraTax platform. While the “E-Services” button previously provided direct access to EmaraTax, this option will be removed from the main navigation bar. Businesses can continue to access the platform through the “Services” dropdown menu on the FTA website. This update is part of the FTA’s ongoing efforts to provide a more intuitive, streamlined, and user-friendly digital experience for taxpayers across the UAE. Introduction The EmaraTax platform is the UAE’s official online portal for managing tax-related obligations, including Corporate Tax, VAT, Excise Tax, registrations, return filings, tax payments, and various other services provided by the Federal Tax Authority. As businesses increasingly rely on EmaraTax for day-to-day tax compliance activities, it is important to stay informed about changes to the platform and website navigation. The latest update does not affect the functionality of EmaraTax itself. Instead, it changes how users access the platform through the FTA website. What Has Changed? The Federal Tax Authority has confirmed that: ✔ The “E-Services” button will be removed from the main navigation bar. ✔ The EmaraTax platform remains fully operational and accessible. ✔ Users should now access EmaraTax through the “Services” dropdown menu available on the FTA website. The objective is to simplify website navigation and improve the overall user experience. How to Access the EmaraTax Platform Follow these simple steps to access EmaraTax: Step 1: Visit the Official FTA Website Go to: www.tax.gov.ae Step 2: Navigate to the Main Menu Locate the “Services” dropdown menu on the website’s main navigation bar. Step 3: Hover Over “Services” A list of available services will appear. Step 4: Select “EmaraTax” Click on “EmaraTax” to access the platform and proceed with your tax-related activities. Why Is EmaraTax Important for UAE Businesses? The EmaraTax platform serves as the primary portal for managing tax compliance in the UAE. Businesses use EmaraTax for: Corporate Tax Services Corporate Tax Registration Corporate Tax Return Filing Tax Payment Management Compliance Updates VAT Services VAT Registration VAT Return Filing VAT Refund Applications VAT Account Management Excise Tax Services Excise Tax Registration Excise Tax Return Submission Excise Tax Compliance Activities Taxpayer Account Management Updating business information Managing user access Reviewing correspondence from the FTA Tracking compliance obligations Common Issues Businesses Can Avoid Changes to website navigation can sometimes create confusion for finance teams and business owners. To avoid delays: Update Internal Procedures Ensure your finance and tax teams are aware of the new access route. Save the Correct Access Path Update any internal manuals, training documents, or bookmarks that reference the old “E-Services” button. Review User Access Confirm that authorized users can still access the EmaraTax platform without interruption. Stay Updated Monitor announcements issued by the Federal Tax Authority to remain informed about future platform enhancements. Key Takeaways The FTA has updated its website navigation structure. The “E-Services” button will be removed from the main navigation bar. EmaraTax remains fully accessible through the “Services” dropdown menu. No changes have been made to EmaraTax functionality. Businesses should update internal guidance and bookmarks accordingly. Staying informed helps avoid unnecessary delays in tax compliance activities. Conclusion The Federal Tax Authority continues to enhance its digital platforms to improve user experience and streamline access to tax services. While the removal of the “E-Services” button represents a minor navigation change, businesses should familiarize themselves with the new access path to ensure uninterrupted access to EmaraTax. Keeping up with such updates is an important part of maintaining effective tax compliance and avoiding operational disruptions. Need Assistance with EmaraTax, VAT, or Corporate Tax? TFAB Accounting & Business Consulting helps businesses across the UAE manage their tax compliance requirements with confidence. Add Your Heading Text Here

UAE Extends E-Invoicing Provider Deadline to October 2026: What Businesses Need to Know

UAE Extends E-Invoicing Provider Deadline to October 2026: What Businesses Need to Know UAE E-Invoicing Update: More Time, But Businesses Should Not Delay Preparation The UAE Ministry of Finance (MoF) has officially extended the deadline for appointing an Accredited Service Provider (ASP) under the UAE e-invoicing framework from 31 July 2026 to 30 October 2026. While this extension offers businesses additional preparation time, the final compliance deadline of 1 January 2027 remains unchanged. For businesses operating in the UAE, this is a critical reminder that digital tax compliance is rapidly becoming a core part of financial operations. Introduction The UAE continues to strengthen its digital tax ecosystem through the implementation of e-invoicing regulations aimed at improving transparency, efficiency, and compliance. As part of the latest regulatory developments, the Ministry of Finance introduced targeted amendments to the e-invoicing framework under Ministerial Decision No. 244 of 2025. One of the most significant updates is the extension of the deadline for businesses with annual revenues exceeding AED 50 million to appoint an Accredited Service Provider (ASP). According to the Ministry, the decision follows: Comprehensive market readiness assessments Business sector feedback Technical integration considerations Pricing and provider availability concerns This move reflects the UAE’s practical and business-friendly approach toward digital transformation. What is the UAE E-Invoicing System? The UAE e-invoicing system is part of the country’s broader digital transformation strategy and tax modernization initiative. The system aims to: Improve invoice standardization Enhance VAT compliance Reduce manual processing Strengthen tax transparency Support real-time digital reporting Under the framework, businesses will be required to issue invoices electronically through approved systems integrated with Accredited Service Providers (ASPs). Extension of ASP Appointment Deadline Previous Deadline : 31 July 2026 Revised Deadline : 30 October 2026 Who is Affected? Businesses with annual revenues exceeding AED 50 million. The Ministry clarified that the final implementation deadline remains : 1 January 2027 This means businesses now have additional time to: Evaluate providers Assess technical readiness Upgrade accounting systems Plan ERP integrations However, businesses should avoid treating this as a reason to postpone preparations entirely. Why Did the UAE Extend the Deadline? The Ministry of Finance highlighted several reasons behind the extension. 1. Market Readiness Many businesses and providers are still preparing their technical infrastructure for full implementation. 2. Need for More Technical Options The UAE wants businesses to have broader access to: Technology solutions Service providers Competitive pricing structures. 3. Business Sector Feedback The extension reflects ongoing dialogue between regulators and the private sector to ensure a smoother transition. Growth of the UAE E-Invoicing Ecosystem The UAE’s e-invoicing ecosystem is rapidly expanding. According to the Ministry: 32 Accredited Service Providers have already been approved Additional providers are in the final stages of accreditation This growth will help create: Greater competition Better service quality Improved pricing flexibility Wider integration capabilities Introduction of the White-Label Framework One of the most important updates is the introduction of a white-label mechanism. What Does This Mean? The framework allows UAE national companies to partner with international service providers. Objectives of the Initiative Knowledge transfer Strengthening local technical capabilities Enhancing service quality Accelerating digital transformation Ensuring compliance with UAE requirements This initiative supports long-term development of the UAE’s digital economy and local technology ecosystem. Practical Impact on Businesses E-invoicing will impact more than just invoice generation. Businesses may need to review: ERP systems Accounting software VAT reporting workflows Invoice approval processes Data security and archiving procedures Example: How Businesses Should Prepare Example 1: Large Trading Company A trading company with revenue above AED 50 million may need: ERP integration ASP evaluation Invoice automation VAT workflow restructuring Example 2: Service-Based Business A consulting company may need: Accounting software upgrades Digital invoice approval processes Integration with tax reporting systems Key Takeaways ASP appointment deadline extended to 30 October 2026 Final implementation deadline remains 1 January 2027 Final implementation deadline remains 1 January 2027 UAE is expanding the e-invoicing provider ecosystem White-label framework introduced to strengthen local capabilities Businesses should begin preparation early to avoid disruptions E-invoicing will impact accounting, ERP, VAT, and compliance systems Conclusion The UAE’s extension of the ASP appointment deadline demonstrates a balanced and business-oriented approach to digital transformation. While businesses now have additional preparation time, the final implementation deadline remains unchanged. Organizations that proactively assess their systems, evaluate providers, and begin implementation planning early will be in a significantly stronger position when e-invoicing becomes mandatory. The transition to digital compliance is no longer optional – it is becoming an essential part of doing business in the UAE. Need Guidance on UAE E-Invoicing Readiness?At TFAB Accounting & Business Consulting, we help businesses:✔ Assess e-invoicing readiness✔ Review accounting and ERP systems✔ Support VAT and Corporate Tax compliance✔ Prepare for digital transformation requirements in the UAE Contact TFAB today to discuss how your business can prepare for the UAE e-invoicing framework efficiently and confidently.

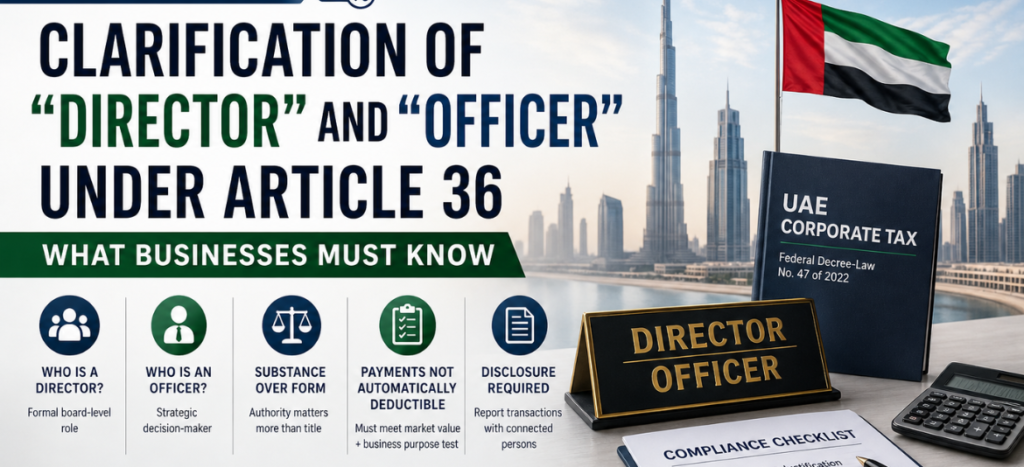

Corporate Tax UAE: Clarification of “Director” and “Officer” Under Article 36 – What Businesses Must Know

Corporate Tax UAE: Clarification of “Director” and “Officer” Under Article 36 – What Businesses Must Know Are Director Payments Tax Deductible in UAE Corporate Tax? Are your Director or management payments truly tax deductible under UAE Corporate Tax? The UAE Federal Tax Authority (FTA) has issued an important clarification that could directly impact how businesses structure compensation, classify roles, and ensure tax compliance. Introduction to UAE Corporate Tax and Connected Persons With the introduction of UAE Corporate Tax under Federal Decree-Law No. 47 of 2022, businesses must ensure that transactions with Connected Persons are properly structured and compliant. A recent Public Clarification from the Federal Tax Authority explains how the terms “Director” and “Officer” should be interpreted under Article 36 of the Corporate Tax Law. This is critical because payments to such individuals are: Not automatically deductible Subject to strict compliance and disclosure rules Understanding Article 36: Payments to Connected Persons Under Article 36(1) of UAE Corporate Tax Law: Payments or benefits to Connected Persons are deductible only if: They reflect market value (arm’s length principle) They are incurred wholly and exclusively for business purposes Additionally, under Article 55: Businesses must disclose such transactions in their tax return if thresholds are exceeded. Who is a “Director” under UAE Corporate Tax? A Director refers to: A person who is part of the Board of Directors, OR A member of an equivalent governing body (e.g., trustees, governors) Important Clarification: A job title alone does NOT make someone a Director. Even if someone is called “Director”: They must be formally part of the governing body Otherwise, they are NOT treated as a Director for tax purposes Who is an “Officer” under UAE Corporate Tax? The term Officer is broader and based on actual authority. An Officer includes individuals who: Have authority to plan, direct, and control business activities Make strategic financial or operational decisions Can enter into agreements or legally bind the company Examples of Officers: CEO CFO General Manager COO Key decision-makers Substance Over Form: A Key Principle The FTA emphasizes a substance-over-form approach. This means: Titles alone are NOT sufficient Actual decision-making authority matters more Even without formal designation, a person can be classified as an Officer This approach aligns with IAS 24 – Related Party Disclosures. Practical Examples (Easy to Understand) ✔ Example 1: General Manager with full operational control is Considered as an Officer. ❌ Example 2: Department Head without decision-making authority is NOT considered as an Officer. ✔ Example 3: HR Head with strategic authority is Considered as an Officer. ❌ Example 4: Employee performing routine tasks is NOT Considered as an Officer. Key Compliance Requirements for UAE Businesses To ensure compliance with UAE Corporate Tax: 1. Market Value Justification Payments must follow arm’s length pricing 2. Proper Classification Clearly identify: Director Officer Other employees 3. Disclosure Requirements Report transactions with Connected Persons in tax filings 4. Documentation Maintain: Employment contracts Role definitions Justification for compensation Key Takeaways “Director” – formal board-level role “Officer” – strategic decision-maker Payments are not automatically deductible Must meet market value + business purpose test Certain transactions require FTA disclosure Substance matters more than designation Conclusion The FTA’s clarification marks a major shift in UAE Corporate Tax compliance. It’s no longer about titles It’s about real authority, structure, and transparency Businesses that fail to align may face: Disallowed expenses Increased tax liability Compliance risks Need Help with Corporate Tax Compliance? Are your Director or management payments aligned with UAE Corporate Tax regulations? Contact TFAB Accounting & Business Consulting today Ensure your structure is compliant, optimized, and risk-free.

How Auditing & Accounting Firms in Dubai Legally Reduce Tax Liability in 2026

How Auditing & Accounting Firms in Dubai Legally Reduce Tax Liability in 2026 In today’s rapidly evolving financial landscape, businesses in Dubai face growing pressure to stay compliant while optimizing their tax strategy. Auditing and accounting firms in Dubai play a crucial role in helping companies reduce tax liability legally through strategic tax planning, VAT optimization, and corporate tax efficiency. Whether you are a startup, SME, or established enterprise, partnering with professional auditing and accounting firms can improve profitability, ensure compliance, and support long-term growth. Businesses in the UAE can legally reduce tax liability through structured financial planning Accounting firms in Dubai help optimize VAT, corporate tax, and deductions Proper planning improves cash flow, compliance, and profitability Choosing the right firm ensures audit readiness and risk reduction Why Tax Optimization Matters in Dubai With the UAE introducing a 9% corporate tax alongside the existing 5% VAT, companies now operate under a dual-layer tax system. Without proper planning, businesses risk: Higher tax outflows Compliance penalties Cash flow disruptions Role of Auditing & Accounting Firms in Tax Planning Professional auditing and accounting firms act as financial strategists, not just bookkeepers. Their services include: 1. Strategic Financial Structuring Advising on business setup (Mainland vs Free Zone) Optimizing revenue streams for tax efficiency Aligning financial reporting with available tax benefits 2. VAT Optimization Techniques Identifying recoverable input VAT Ensuring correct VAT classification: standard, zero-rated, or exempt Preventing overpayment due to misclassification 3. Corporate Tax Efficiency Planning Claiming allowable deductions Structuring expenses to reduce taxable income Ensuring full compliance with UAE tax laws Legal Ways to Reduce Tax Liability in the UAE Maximizing Allowable Deductions Businesses can legally reduce taxable income by claiming: Operating expenses: salaries, office rent, utilities, and admin costs Depreciation and asset planning: capital asset allocation strategies Transfer pricing compliance for international operations Free Zone vs Mainland Tax Benefits Free Zones: may offer tax incentives under specific conditions Mainland Businesses: enjoy operational flexibility and broader market access Ensuring Compliance While Saving Tax Auditing firms help businesses stay audit-ready by: Accurate tax filings and timely submissions Maintaining proper documentation Reducing risk of penalties, audits, and legal complications How Professional Firms Ensure Compliance While Saving Tax FTA Regulations and Risk Management Auditing firms ensure: Accurate tax filings Timely submissions Proper documentation This reduces the risk of: Penalties Audits Legal complications Audit-Ready Financial Reporting Maintaining clean financial records ensures: Smooth audits Better investor confidence Improved financial transparency Choosing the Right Auditing & Accounting Firm in Dubai Key Qualities to Look For UAE tax expertise (VAT + Corporate Tax) Proven industry experience Strong compliance record Advisory and consulting capabilities Questions to Ask Before Hiring How do you approach tax optimization? Can you support audit readiness? Which industries do you specialize in? Do you provide ongoing compliance support? Benefits of Expert Accounting Firms in Dubai Cost Savings – Optimized tax planning reduces unnecessary expenses Improved Financial Planning – Better budgeting and cash flow management Business Growth – More capital available for expansion Common Mistakes Businesses Make Ignoring tax planning until year-end Misclassifying VAT transactions Failing to maintain proper documentation Not seeking expert advice How Businesses Reduce Tax Legally in Dubai Businesses can reduce tax legally in Dubai by claiming allowable expenses and deductions, optimizing VAT recovery, structuring operations efficiently, and partnering with professional auditing and accounting firms to ensure full compliance with UAE tax laws. Conclusion Tax optimization is no longer optional it’s essential for sustainable business growth in Dubai. Partnering with experienced auditing and accounting firms like TFAB allows businesses to reduce tax liability legally, maintain compliance, and improve financial efficiency. By leveraging professional guidance, companies can minimize risks, improve cash flow, and unlock new opportunities for long-term profitability and expansion. FAQs Can accounting firms help reduce corporate tax in the UAE? Yes. They identify deductions, optimize financial structures, and ensure compliance to legally reduce tax liability. Is tax optimization legal in Dubai? Yes. Tax optimization is legal when businesses follow UAE tax laws and FTA regulations. What is the role of auditing firms in tax compliance? They ensure accurate financial reporting, timely submissions, and audit readiness. Do SMEs need accounting firms in Dubai? Yes. SMEs benefit significantly from expert guidance in VAT, corporate tax, and financial planning. Yes. They identify deductions, optimize financial structures, and ensure compliance to legally reduce tax liability. Yes. Tax optimization is legal when businesses follow UAE tax laws and FTA regulations. They ensure accurate financial reporting, timely submissions, and audit readiness. Yes. SMEs benefit significantly from expert guidance in VAT, corporate tax, and financial planning.

Top Auditing & Accounting Firms in Dubai (2026): Services, Pricing & How to Choose

Top Auditing & Accounting Firms in Dubai (2026): Services, Pricing & How to Choose Choosing the Top Auditing & Accounting Firms in Dubai is a critical decision that directly impacts your business compliance, financial clarity, and long-term growth. With evolving UAE regulations, VAT complexities, and increased scrutiny on financial reporting, businesses are no longer just looking for accountants; they need strategic financial partners. This guide breaks down the services, pricing, and selection criteria to help you choose the right firm in 2026. What Defines the Top Auditing & Accounting Firms in Dubai? Not all firms deliver the same value. The top-performing firms typically offer: End-to-end accounting and bookkeeping services in Dubai Advanced VAT services in Dubai with compliance expertise Independent internal audit services in UAE Industry-specific financial advisory Cloud-based accounting and real-time reporting Core Services Offered by Leading Firms 1. Accounting and Bookkeeping Services These services form the backbone of financial management: Daily transaction recording Financial statement preparation Cash flow monitoring Payroll processing 2. VAT Services in Dubai With strict UAE tax regulations, VAT errors can be costly. Top firms provide: VAT registration & deregistration Filing & return submission VAT audit support Compliance advisory 3. Internal Audit Services in UAE Internal audits evaluate your financial systems and risk exposure. Includes: Risk assessment Internal control evaluation Fraud detection Process improvement 4. External Audit & Assurance Mandatory for many companies in Dubai, especially free zone entities. Financial audit reports IFRS compliance Third-party verification 5. Financial Advisory & CFO Services Modern firms go beyond accounting: Budgeting & forecasting Business restructuring Cost optimization strategies How to Choose the Right Accounting Firm in Dubai Industry Experience Choose a firm that has experience in your specific industry. This ensures they understand your financial challenges, compliance requirements, and reporting standards. Compliance Expertise Ensure the firm is well-versed in UAE financial regulations, VAT laws, and audit requirements to help you avoid penalties and maintain accuracy. Technology & Tools Look for firms that use cloud accounting software, real-time dashboards, and automated reporting systems for better efficiency and transparency. Transparency in Pricing Select a firm that provides clear pricing structures with no hidden charges. A well-defined scope of services prevents confusion later. Reputation & Client Reviews Check testimonials, case studies, and client feedback. Firms with strong reputations and long-term clients are generally more reliable. Common Mistakes to Avoid When Hiring an Accounting Firm Choosing based on low cost only Ignoring VAT expertise Not checking compliance credentials Lack of service-level agreement (SLA)a What are the top auditing and accounting firms in Dubai known for? The top auditing and accounting firms in Dubai are known for providing comprehensive services such as bookkeeping, VAT compliance, internal audits, and financial advisory while ensuring regulatory compliance and cost efficiency. Why Businesses in Dubai Prefer Outsourced Accounting Firms Access to expert professionals Reduced operational costs Better compliance with UAE laws Scalable financial solutions Conclusion Choosing the Top Auditing & Accounting Firms in Dubai is not just about compliance it’s about building a financially strong and scalable business. With the right partner, you gain expert insights, reduce operational costs, and stay ahead of regulatory challenges. If you’re looking for reliable, result-driven accounting and bookkeeping services in Dubai, VAT services in Dubai, and internal audit services in UAE, TFAB offers tailored solutions designed to support your business growth with accuracy and compliance. Get in touch with TFAB today to streamline your financial operations and make smarter business decisions. FAQs What are the top auditing & accounting firms in Dubai? They are firms offering comprehensive financial services including accounting, VAT, audit, and advisory with proven expertise and compliance knowledge. How much do accounting services cost in Dubai? Costs range from AED 1,000 to AED 8,000 monthly depending on business size and service requirements. Are VAT services mandatory in Dubai? Yes, VAT compliance is mandatory for eligible businesses under UAE law. Why should businesses outsource accounting services? Outsourcing reduces costs, improves accuracy, and ensures compliance with regulations. What is included in internal audit services in UAE? It includes risk assessment, internal control review, and compliance evaluation. They are firms offering comprehensive financial services including accounting, VAT, audit, and advisory with proven expertise and compliance knowledge. Costs range from AED 1,000 to AED 8,000 monthly depending on business size and service requirements. Yes, VAT compliance is mandatory for eligible businesses under UAE law. Outsourcing reduces costs, improves accuracy, and ensures compliance with regulations. It includes risk assessment, internal control review, and compliance evaluation.

Cost of Accounting Services in Dubai (2026 Guide)

Cost of Accounting Services in Dubai (2026 Guide) Understanding the cost of accounting services in Dubai is essential for businesses aiming to stay compliant, profitable, and scalable in the UAE’s evolving financial landscape. Whether you’re a startup, SME, or large enterprise, knowing how pricing works helps you make informed decisions and avoid unnecessary expenses. In this guide, we break down actual pricing, cost factors, and expert insights to help you choose the right accounting partner. Accounting services in Dubai typically cost AED 500–AED 5,000+/month Pricing depends on business size, transactions, and services required Outsourcing is often more cost-effective than hiring in-house Choosing the right firm ensures compliance and long-term savings How Much Do Accounting Services Cost in Dubai? The cost of accounting services in Dubai ranges from AED 500 to AED 5,000+ per month, depending on business size, transaction volume, and required services such as bookkeeping, VAT filing, and corporate tax compliance. Key Factors That Affect Accounting Costs Understanding these factors helps you estimate your actual cost: 1. Business Size & Transactions More transactions = more bookkeeping work = higher cost. 2. Scope of Services Basic bookkeeping costs less than full-service accounting, which may include: VAT registration & filing Corporate tax compliance Payroll processing Financial reporting 3. Industry Complexity Industries like healthcare, finance, and e-commerce require stricter compliance. 4. Frequency of Reporting Monthly reporting costs more than quarterly or annual reporting. 5. Software & Automation Firms using tools like QuickBooks or Zoho Books may charge differently based on automation. Types of Accounting Services in Dubai Businesses in Dubai typically require: Bookkeeping Services Recording daily financial transactions VAT Services VAT registration VAT return filing Corporate Tax Services Ensuring compliance with UAE corporate tax laws Audit Support Preparation for financial audits Financial Reporting Profit & loss statements, balance sheets In-House vs Outsourced Accounting – Cost Comparison In-House Accounting: Salary: AED 4,000 – AED 10,000/month Additional costs: visa, insurance, office space Outsourced Accounting: Cost: AED 1,000 – AED 5,000/month No overhead expenses Why Outsourcing Accounting Services in Dubai is Cost-Effective Outsourcing is a growing trend due to: Lower operational costs Access to experienced professionals Compliance with UAE regulations Scalable services Future Trends Affecting Accounting Costs in Dubai (2026) Corporate tax implementation Increased compliance requirements Automation in accounting How to Choose the Right Accounting Firm in Dubai Before selecting a firm, consider: Experience in UAE regulations Transparent pricing structure Range of services offered Client reviews and reputation Pro Tips to Reduce Accounting Costs Automate invoicing and bookkeeping Choose bundled service packages Maintain organized financial records Avoid last-minute tax filing Conclusion The cost of accounting services in Dubai varies depending on your business size, operational complexity, and the range of services required. While basic bookkeeping may appear affordable initially, investing in comprehensive accounting solutions ensures long-term financial accuracy, regulatory compliance, and sustainable business growth. Businesses that prioritize expertise over just pricing often achieve better financial outcomes and avoid costly mistakes. Partnering with a trusted firm like TFAB allows businesses to access reliable, cost-effective accounting services tailored to their needs, helping them stay compliant while optimizing overall financial performance in Dubai’s competitive market. FAQs What is the average cost of accounting services in Dubai? AED 500 to AED 5,000+ per month depending on business needs. Is outsourcing accounting cheaper than hiring in-house? Yes, outsourcing can reduce costs by up to 50% while ensuring compliance. Do accounting firms in Dubai offer customized pricing? Yes, most firms provide tailored packages based on business requirements. What services are included in accounting packages? Bookkeeping, VAT filing, payroll, financial reporting, and tax compliance. AED 500 to AED 5,000+ per month depending on business needs. Yes, outsourcing can reduce costs by up to 50% while ensuring compliance. Yes, most firms provide tailored packages based on business requirements. Bookkeeping, VAT filing, payroll, financial reporting, and tax compliance.

What Happens During a Financial Audit in Dubai? A Complete Guide by Auditing & Accounting Firms in Dubai

What Happens During a Financial Audit in Dubai? A Complete Guide by Auditing & Accounting Firms in Dubai A financial audit in Dubai plays a key role in maintaining accurate financial records, ensuring regulatory compliance, and improving business transparency. In a fast-growing and competitive market, businesses need structured financial processes to stay compliant and make confident decisions. Professional accounting & auditing firms in Dubai help organizations evaluate financial performance, identify risks, and strengthen internal controls. When approached strategically, a financial audit becomes more than a requirement it becomes a foundation for sustainable growth. What Happens During a Financial Audit in Dubai? A financial audit in Dubai is a structured process where financial records are reviewed, internal controls are assessed, and compliance with UAE regulations is verified. The goal is to ensure that financial statements are accurate, reliable, and aligned with reporting standards. Why Financial Audits Are Important in Dubai Financial audits are essential for businesses operating in Dubai due to strict regulatory and financial reporting requirements. Ensure compliance with UAE laws and Free Zone regulations Strengthen credibility with investors, banks, and stakeholders Detect financial errors and reduce fraud risks Improve internal controls and operational efficiency Types of Financial Audits in Dubai Businesses may require different types of audits depending on their operations and legal structure. External Audit: Conducted by independent auditors for compliance and reporting Internal Audit: Focuses on improving internal systems and risk management Statutory Audit: Mandatory for many Free Zone companies VAT Audit: Ensures compliance with regulations set by the Federal Tax Authority Forensic Audit: Investigates financial discrepancies or fraud Step-by-Step Financial Audit Process in Dubai 1. Audit Engagement and Planning The process begins with appointing a licensed audit firm. The scope, timeline, and key risk areas are defined to ensure an efficient audit process. 2. Evaluation of Internal Controls Auditors review financial systems, approval workflows, and documentation practices to identify potential weaknesses. 3. Document Collection and Review Businesses must provide essential financial records, including: Financial statements Bank statements VAT returns Invoices and receipts Payroll records Organized documentation helps streamline the audit process. 4. Audit Fieldwork and Testing This is the core phase where detailed checks are performed. Auditors: Verify financial transactions Perform sampling checks Reconcile accounts Validate financial data accuracy 5. Compliance Verification Auditors ensure compliance with: UAE Commercial Companies Law VAT regulations governed by the Federal Tax Authority Free Zone authority requirements 6. Audit Findings and Adjustments Any discrepancies or gaps are identified, including: Financial reporting errors Missing documentation Compliance issues Corrections are recommended to improve accuracy. 7. Audit Report Issuance The final audit report reflects the auditor’s opinion: Unqualified (Clean Report) Qualified Report Adverse Report Disclaimer of Opinion 8. Post-Audit Advisory Audit firms also provide valuable recommendations, such as: Improving internal controls Risk management strategies Tax and VAT compliance guidance Audit Standards and Regulations in Dubai Financial audits in Dubai follow internationally recognized frameworks to ensure reliability and transparency: International Financial Reporting Standards (IFRS) International Standards on Auditing (ISA) UAE Commercial Companies Law VAT regulations under the Federal Tax Authority Who Needs a Financial Audit in Dubai? Free Zone companies SMEs seeking investment or funding Companies applying for bank loans Businesses requiring regulatory compliance Common Audit Mistakes Businesses Make Poor financial documentation Lack of proper VAT reconciliation Weak internal controls Delayed or inconsistent bookkeeping How to Prepare for a Financial Audit in Dubai Proper preparation ensures a smooth and efficient audit process: Maintain accurate and updated bookkeeping Reconcile accounts regularly Ensure VAT compliance Organize financial records Conduct internal audits periodically Risks of Not Conducting a Financial Audit Skipping financial audits can lead to serious consequences: Regulatory penalties and fines Increased risk of fraud Loss of investor confidence Difficulty securing loans Poor financial decision-making Benefits of Working with Professional Audit Firms Partnering with experienced audit professionals offers several advantages: Accurate and reliable financial reporting Strong compliance with UAE regulations Improved internal processes Better risk management Enhanced business credibility How Financial Audits Support Business Growth A financial audit is not just a compliance requirement it can also drive growth by: Identifying cost-saving opportunities Improving financial planning and forecasting Building trust with investors Supporting expansion and scaling strategies Choosing the Right Auditing & Accounting Firms in Dubai Selecting the right audit partner is crucial. Consider the following: Experience with UAE regulations Industry-specific expertise Strong compliance knowledge Advisory and consulting capabilities Conclusion A financial audit in Dubai is a valuable process that helps businesses maintain compliance, improve transparency, and strengthen financial performance. With the right approach, audits can provide meaningful insights that support better decision-making and long-term growth. Working with reliable accounting & auditing firms in Dubai ensures your audit is handled with accuracy and professionalism. If you’re looking for a trusted partner, TFAB offers expert auditing, VAT compliance, and financial advisory services tailored to your business needs. Contact TFAB today to make your audit process smooth, compliant, and effective FAQs What happens during a financial audit in Dubai? A financial audit involves reviewing financial records, assessing internal controls, verifying compliance, and issuing an audit report. Why hire auditing & accounting firms in Dubai? They help ensure compliance, improve accuracy, reduce risks, and enhance business credibility. Is a financial audit mandatory in Dubai? Yes, especially for Free Zone companies and regulated businesses. How long does a financial audit take? Typically 1–4 weeks depending on the size and complexity of the company. What documents are required for an audit? Financial statements, VAT returns, bank records, invoices, and payroll data. What is the cost of audit services in Dubai? Costs vary based on business size, transaction volume, and complexity. What happens if a company fails an audit? It may face compliance issues, penalties, or required financial corrections. Can small businesses benefit from audits? Yes, audits improve financial accuracy, efficiency, and credibility. A financial audit involves reviewing financial records, assessing internal controls, verifying compliance, and issuing an audit report. They help ensure compliance, improve accuracy, reduce risks, and enhance business credibility. Yes, especially for Free Zone companies and regulated businesses. Typically

Why Outsourced Accounting and Bookkeeping Services in Dubai Are More Cost Effective Than In-House Teams

Why Outsourced Accounting and Bookkeeping Services in Dubai Are More Cost Effective Than In-House Teams In today’s competitive business landscape, companies in Dubai are under constant pressure to optimize costs while maintaining financial accuracy and compliance. Whether you’re a startup, SME, or growing enterprise, managing finances efficiently is non-negotiable. This is where accounting and bookkeeping services in Dubai play a crucial role. Traditionally, businesses relied on in-house accounting teams. However, a significant shift is happening. More companies are now turning to top accounting firms in Dubai and auditing & accounting firms in Dubai to streamline operations, reduce costs, and ensure regulatory compliance. But is outsourcing truly more cost-effective than maintaining an in-house team? Let’s break it down with data-driven insights and real-world advantages What Are Outsourced Accounting and Bookkeeping Services? Outsourced accounting refers to hiring external experts or firms to manage financial tasks such as Bookkeeping and financial reporting Payroll processing VAT services in Dubai Tax compliance and filing Internal audit services in UAE These services are typically offered by specialized auditing & accounting firms in Dubai equipped with advanced tools and regulatory expertise. Cost Breakdown: Outsourced vs In-House Accounting 1. Salary & Benefits Costs An in-house accountant in Dubai comes with: Monthly salary (AED 5,000 – AED 15,000+) Employee benefits (insurance, visa, gratuity) Training and onboarding costs Outsourcing Advantage: You pay only for the services you need no hidden HR or administrative costs. 2. Infrastructure & Technology Costs In-house teams require: Accounting software licenses Office space and IT infrastructure Data security systems Outsourcing Advantage: Top firms already use advanced cloud-based accounting systems, eliminating your need to invest in expensive tools. 3. Compliance & Regulatory Risks Dubai has strict financial regulations, including VAT compliance. Mistakes can lead to: Heavy penalties Legal complications Reputation damage Outsourcing Advantage: Professional firms specializing in VAT services in Dubai ensure accurate filing and compliance with UAE laws. 4. Scalability & Flexibility In-house teams are fixed resources. Hiring during growth = more cost Downsizing = HR complications Outsourcing Advantage: Scale services up or down based on your business needs without long-term commitments. Data-Driven Insight: Why Businesses Are Shifting Companies can reduce operational costs by 30%–60% through outsourcing SMEs report higher efficiency and fewer compliance errors Faster financial reporting improves decision-making This is why many businesses prefer working with top accounting firms in Dubai instead of building internal teams. Key Benefits of Outsourcing Accounting in Dubai 1. Access to Expert Knowledge Outsourcing gives you access to: Certified accountants Tax consultants 2. Focus on Core Business Activities Instead of managing accounts, you can focus on: Growth strategies Customer acquisition Market expansion 3. Improved Accuracy & Reduced Errors Professional firms follow standardized processes, reducing: Human errors Financial discrepancies Compliance risks 4. Advanced Technology & Automation Outsourced firms use: Cloud accounting AI-driven reporting Real-time dashboards In-House Accounting: When Does It Make Sense? To be precise, outsourcing isn’t always the perfect solution. You might consider in-house accounting if: You are a large enterprise with complex internal operations You require full-time financial control daily You handle highly sensitive financial data internally How to Choose the Right Accounting Partner in Dubai When selecting from auditing & accounting firms in Dubai, consider: Industry Experience Choose firms with experience in your niche. Compliance Expertise Ensure they specialize in VAT services in Dubai and UAE regulations. Technology Stack Look for firms using cloud-based accounting tools. Transparency & Pricing Avoid hidden costs opt for clear pricing models. Client Reviews & Reputation Top firms will have strong testimonials and proven case studies. Conclusion Outsourcing accounting and bookkeeping services in Dubai is no longer just a cost cutting tactic it’s a strategic move that empowers businesses with greater efficiency, regulatory compliance, and access to specialized financial expertise without the overhead of an in-house team. Whether you’re a startup looking to scale or an established company aiming to optimize operations, working with the right financial partner can make a measurable difference. TFAB, as a trusted service provider, supports businesses with reliable, compliant, and scalable accounting solutions tailored to the UAE market. If you’re ready to simplify your financial processes and focus on growth, now is the ideal time to partner with experts who understand your business needs and can guide you toward long-term financial stability. FAQs What are accounting and bookkeeping services in Dubai? They include financial record management, VAT filing, payroll processing, and compliance handled by professional firms. Why are outsourced accounting services popular in Dubai? Due to cost savings, regulatory complexity, and access to expert financial professionals. How much do accounting services cost in Dubai? Costs vary depending on business size but are generally lower than hiring full-time staff. Are VAT services included in outsourced accounting? Yes, most firms provide complete VAT registration, filing, and compliance services. Can outsourcing replace internal audit functions? Yes, many firms offer internal audit services in UAE as part of their packages They include financial record management, VAT filing, payroll processing, and compliance handled by professional firms. Due to cost savings, regulatory complexity, and access to expert financial professionals. Costs vary depending on business size but are generally lower than hiring full-time staff. Yes, most firms provide complete VAT registration, filing, and compliance services. Yes, many firms offer internal audit services in UAE as part of their packages

TRN Registration and Deactivation in the UAE: Complete Guide (2026)

TRN Registration and Deactivation in the UAE: Complete Guide (2026) The United Arab Emirates is known for its business-friendly environment, but companies operating in the country must comply with tax regulations introduced after the implementation of Value Added Tax (VAT) in 2018. One of the most important requirements for VAT compliance is obtaining a Tax Registration Number (TRN). Issued by the Federal Tax Authority (FTA), the TRN is a unique identifier that allows businesses to legally charge VAT, file tax returns, and claim input tax credits. Without a valid TRN, companies cannot participate fully in the UAE VAT system and may face penalties. Whether you are a startup, established enterprise, or accounting professional, understanding TRN registration and deactivation in the UAE is essential for maintaining compliance and smooth financial operations. Understanding the Role of TRN in the UAE Tax System A Tax Registration Number (TRN) is a 15-digit number assigned to businesses registered for VAT in the UAE. It acts as an official identifier used in tax invoices, VAT returns, financial reporting, and communications with the Federal Tax Authority. The introduction of VAT significantly transformed financial compliance requirements for companies operating in the UAE. Businesses must now ensure accurate tax documentation, periodic filings, and proper accounting practices. The TRN plays a central role in enabling these obligations. According to FTA reports, over 300,000 UAE businesses held a valid TRN in 2025, demonstrating how essential VAT registration has become for companies operating across Dubai, Abu Dhabi, Sharjah, and other emirates. A registered TRN allows businesses to: Legally charge VAT on taxable goods and services Claim VAT refunds on eligible business expenses Issue compliant tax invoices File VAT returns with the Federal Tax Authority Maintain transparency during audits and financial reviews For companies involved in local trade, imports, exports, or services within the UAE, the TRN effectively serves as their tax identity in the national VAT ecosystem. VAT Thresholds and Eligibility for TRN Registration Not every business operating in the UAE must register for VAT immediately. The Federal Tax Authority established specific turnover thresholds that determine whether VAT registration is mandatory or voluntary. Mandatory Registration A company must register for VAT if the total value of taxable supplies and imports exceeds AED 375,000 within a 12-month period or is expected to exceed this threshold soon. Businesses that fail to register despite crossing this threshold may face administrative penalties and compliance investigations. Voluntary Registration Companies with taxable supplies or expenses exceeding AED 187,500 annually can opt for voluntary VAT registration. This option is particularly useful for: Startups preparing for rapid growth Businesses working with VAT-registered suppliers Companies planning to claim input VAT credits Firms involved in international trade Voluntary registration often improves business credibility and financial transparency, especially when dealing with corporate clients and government contracts. Who Should Apply for a TRN in the UAE? VAT registration applies to many businesses operating in the UAE. Companies that typically need TRN registration include: Corporate companies such as LLCs and private firms whose annual turnover exceeds the VAT threshold. Free zone businesses conducting taxable activities in mainland UAE or dealing with VAT-registered companies. Service providers including consultancies, marketing agencies, IT firms, and professional services. Importers and exporters involved in international trade subject to UAE VAT regulations. E-commerce businesses selling goods or services online within the UAE. Step-by-Step Process for TRN Registration in the UAE Registering for a TRN is completed through the Federal Tax Authority’s e-Services portal. While the process is relatively straightforward, businesses must ensure all documentation and financial details are accurate. Step 1: Gather Required Documents Before starting the application, companies should prepare key documents such as: Trade license copy Emirates ID of the owner or partners Passport copies of shareholders Company bank account details Business contact information Financial records showing turnover or expected revenue Accurate documentation speeds up the approval process and reduces the likelihood of application rejection. Step 2: Create an Account on the FTA Portal Businesses must register on the FTA e-Services portal to access the VAT registration form. This step involves creating login credentials, verifying email information, and entering company details. Step 3: Complete the VAT Registration Form The online application requires detailed business information, including: Company structure and legal status Nature of business activities Financial turnover details Import and export activities Authorized signatory information Applicants must also upload supporting documents to validate the information provided. Step 4: Application Review by the Federal Tax Authority Once the application is submitted, the FTA reviews the data and documentation. If additional clarification is required, the authority may request further information before approving the application. Step 5: Receive Your TRN After approval, the business receives its 15-digit TRN via email. This number must then appear on all tax invoices and VAT-related documents. In most cases, the entire registration process takes 5 to 10 business days. Benefits of TRN Registration for Businesses Benefits of TRN Registration for BusinessesWhile procedures may vary depending on the case, the typical process involves the following steps: 1. Log in to the FTA Portal Access your previous account on the FTA e-Services portal using the credentials associated with the deregistered TRN. 2. Submit a Reactivation Request Choose the option to request reactivation rather than new registration. 3. Provide Updated Business Information You may need to submit: Trade license Financial statements Proof of resumed activities Bank details Expected taxable turnover 4. Upload Supporting Documents Additional documentation may be requested to justify reactivation. 5. FTA Review and Approval The authority will assess your eligibility and compliance history before reactivating the TRN. TRN Deactivation and VAT Deregistration in the UAE While VAT registration is essential for many businesses, there are circumstances where TRN deactivation or VAT deregistration becomes necessary. Businesses must apply for deregistration if they stop conducting taxable activities or if their revenue drops below mandatory thresholds. Common Reasons for TRN Deregistration Several situations may require businesses to deactivate their TRN: Business closure or liquidation Annual taxable turnover falling below the mandatory threshold Company mergers or restructuring Change in

VAT Deregistration in the UAE: How to Reactivate Your Previous Registration Instead of Applying Again

VAT Deregistration in the UAE: How to Reactivate Your Previous Registration Instead of Applying Again If your business or individual tax profile has been deregistered in the UAE, you may assume that the only solution is to submit a brand-new registration. However, the Federal Tax Authority (FTA) requires a different approach. If a natural or juridical person has been deregistered and needs to register again, they must request reactivation of the previous registration number rather than apply for a new one. Understanding this rule is critical for businesses operating in the UAE, especially those dealing with VAT compliance. In this guide, we explain what deregistration means, why reactivation is required, and how expert support from TFAB can help you stay compliant. What Does VAT Deregistration Mean in the UAE? VAT deregistration occurs when the FTA cancels your Tax Registration Number (TRN). This may happen voluntarily or mandatorily depending on your business circumstances. Common Reasons for Deregistration Business closure or liquidation Taxable supplies falling below the mandatory threshold Change in business activity Failure to meet compliance requirements Mergers or restructuring Long periods of inactivity Once deregistered, your TRN becomes inactive, meaning you are no longer authorized to charge VAT or submit VAT returns. Natural Person vs. Juridical Person: Who Does This Apply To? The rule applies to both: Natural Persons An individual conducting business in their own name (e.g., freelancers, sole proprietors). Juridical Persons Legally recognized entities such as: LLCs Corporations Partnerships Free zone companies Branches of foreign companies Regardless of category, the original registration must be reactivated not replaced. Why You Cannot Apply for a New Registration The FTA maintains a centralized tax identity system. Each taxpayer is assigned a unique TRN that links to historical filings, compliance records, penalties, and financial data. Applying for a new registration instead of reactivation can: Cause application rejection Trigger compliance audits Delay business operations Create duplicate records Lead to penalties for incorrect filings Reactivation ensures continuity and transparency in the tax system. When Should You Request Reactivation? You must reactivate your previous VAT registration if: Your business resumes operations after closure Your taxable supplies exceed the registration threshold again A temporary suspension ends You restart trading after restructuring Your deregistration was administrative or due to inactivity Timing is crucial. Delays can result in fines or non-compliance issues. Step-by-Step: How to Reactivate a Deregistered VAT Registration While procedures may vary depending on the case, the typical process involves the following steps: 1. Log in to the FTA Portal Access your previous account on the FTA e-Services portal using the credentials associated with the deregistered TRN. 2. Submit a Reactivation Request Choose the option to request reactivation rather than new registration. 3. Provide Updated Business Information You may need to submit: Trade license Financial statements Proof of resumed activities Bank details Expected taxable turnover 4. Upload Supporting Documents Additional documentation may be requested to justify reactivation. 5. FTA Review and Approval The authority will assess your eligibility and compliance history before reactivating the TRN. What Happens After Reactivation? Once approved: Your original TRN becomes active again You can resume charging VAT VAT return obligations restart Compliance deadlines apply immediately Businesses should be prepared to file returns from the reactivation date onward. Risks of Ignoring Reactivation Requirements Operating without proper VAT registration can expose businesses to significant penalties in the UAE. Potential Consequences Administrative fines Backdated tax liabilities Suspension of business activities Legal complications Damage to reputation Ensuring correct reactivation protects your business from costly mistakes. How TFAB Helps Businesses Stay Compliant Navigating VAT regulations in the UAE can be complex, especially when dealing with deregistration and reactivation. Professional guidance ensures accuracy and speed. TFAB provides end-to-end VAT compliance support, including: Assessment of eligibility for reactivation Preparation and submission of FTA applications Documentation review Communication with tax authorities Ongoing VAT compliance and filing services Advisory on avoiding penalties With expert assistance, businesses can resume operations smoothly without regulatory risk. Special Considerations for UAE Businesses Free Zone Companies Free zone entities must confirm whether they operate within designated zones and how VAT applies before reactivation. Group Registrations If part of a VAT group, reactivation may require restructuring of group status. Businesses with Outstanding Liabilities Unpaid penalties or returns may need resolution before approval. Need Help Reactivating Your VAT Registration? If your business has been deregistered and you need to become VAT-registered again, professional guidance can save time and prevent costly errors. TFAB offers expert VAT reactivation services in the UAE from application to approval and ongoing compliance. Contact TFAB today to ensure your business returns to full regulatory compliance smoothly and confidently. Conclusion: Reactivation Is the Only Correct Path If your VAT registration in the UAE has been deregistered, applying for a new registration is not the correct solution. The FTA requires you to reactivate your previous registration number, ensuring continuity and proper tax oversight. Failing to follow this process can lead to delays, fines, and compliance issues. Businesses planning to resume operations should act quickly and seek expert assistance. Frequently Asked Questions Can I get a new TRN after deregistration? No. The FTA requires reactivation of the original TRN instead of issuing a new one. How long does reactivation take? Processing time varies depending on documentation and compliance status but typically ranges from a few days to several weeks. Do I need to pay penalties before reactivation? In many cases, outstanding liabilities must be cleared first. Can a closed company reactivate VAT registration? Only if the business resumes taxable activities and meets eligibility criteria. No. The FTA requires reactivation of the original TRN instead of issuing a new one. Processing time varies depending on documentation and compliance status but typically ranges from a few days to several weeks. In many cases, outstanding liabilities must be cleared first. Only if the business resumes taxable activities and meets eligibility criteria.